Hello readers, welcome to my first blog post. Well, I can already imagine all the stereotyping faces when one reads the title. No, I don’t get financial support from parents. No, I don’t live life without financial worries.

I managed to buy my first house at the age of 24 (23 years and 9 months to be exact) with less than RM5,000 savings in the bank, yes, all thanks to Malaysia government. ✌️

Two of the various government’s first-house ownership aids that I have taken advantage of:

1 | RUMAWIP / Residensi Wilayah

What is it?

An affordable housing scheme dedicated to low and middle income earners working or living in Federal Territory of which the properties are affordably priced – up to RM300,000. However, you cannot sell the property within 10 years, counting from the building’s construction period.

Who is eligible?

Malaysians, aged 21 or above, working or living in Federal Territory, with monthly gross income below RM10,000 (for single applicants) or RM15,000 (for married applicants), and do not own any house in the Federal Territory.

How to apply?

- Choose your dream house from the list of available housing projects here. TIP: Find out more about the property at Forum Lowyat‘s dedicated thread.

- Register an account and click the “apply” button on the project’s page.

- Prepare the required documents in soft-copy formats (.jpeg / .png / .pdf) and upload them to the portal under your account.

- Just wait while your application is being processed. Log on to check your application status from time to time.

- If the status shows “Tawaran Unit“, then congratulations, you are one step closer in owning the house!

What’s next?

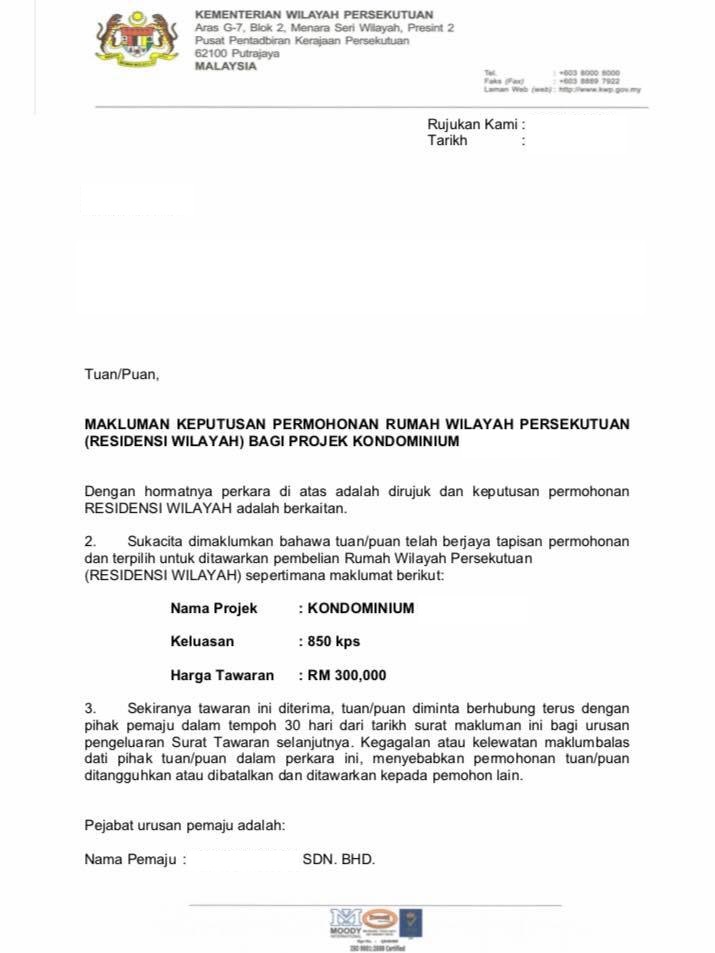

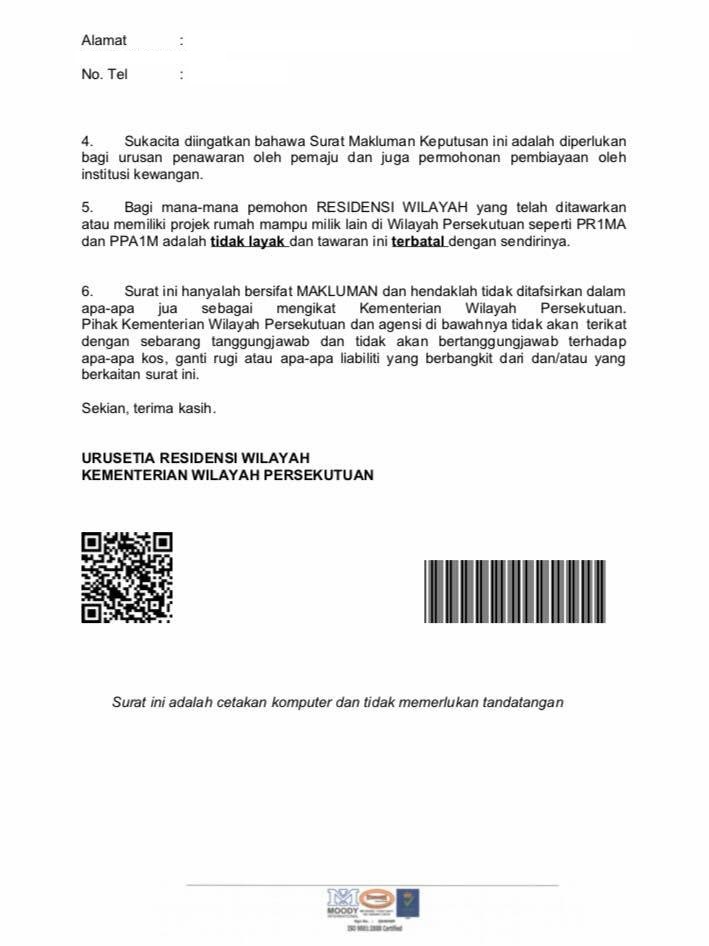

You should be able to see an offer letter named in Bahasa Melayu “Surat Berjaya Tapisan” either in the portal’s account or your email box. At this point, you will be dealing directly with the DEVELOPER and not RUMAWIP authority anymore.

sample of the offer letter

some info has been erased

The first thing you need to do is calling the developer and asking when is the ballot day and what you need to prepare beforehand.

The Balloting Day

To prepare: A cheque or bank draft amounting to

- 10% of the property price which will eventually serve as down payment (for 90% or below loan borrowers) OR

- stipulated amount of booking fees (for 100% loan borrowers)

To bring: Original IC, offer letter and cheque/bank draft

The processes:

- Register at designated counter to get a ballot number. If you get “39” that means you are the 39th person to draw the unit number.

- Draw a random piece of paper from the box prepared when it’s your turn.

- Decide to take it or leave it.

- 👍 SATISFY -> Sign SPA (Sales Purchase Agreement) on the spot with panel lawyers (law firms appointed by the developer). Proceed with loan application with panel bankers (banks appointed by the developer). NOTE: You are free to appoint your own, preferred law firm and bank that are not in the panel list.

- 👎 NOT SATISFY -> Check with developer if you can re-draw (normally cannot), if you wish. Otherwise, give it a pass. You can apply other projects of your choice and go through the similar processes again.

2 | Skim Rumah Pertamaku

What is it?

First home ownership scheme that assists eligible Malaysians in buying their first house without having the need to pay a down payment by allowing them to obtain up to 110% financing from the participating banks.

This scheme is applicable to all residential properties in both primary and secondary markets, be it under construction or already completed, located in Malaysia, pricing up to RM500,000 only. Buyers are required to reside in the property.

Who is eligible?

Malaysians, who are first time house buyers and have no record of impaired financing for the past 12 months. For property priced up to

- RM500,000 – monthly gross income should be below RM5,000 (for single applicants) or RM10,000 (for joint* applicants – max. earning RM5,000 each)

- RM300,000 – monthly gross income should be below RM5,000 (for both single and joint* applicants)

*spouse/parents/children/siblings

How to apply?

Application can be made at any branch of the participating banks listed here.

So yes, I borrowed 100% loan, of course, at slightly higher interest rate (my case: +0.25%) if compared to 90% loan but I own a house at my favorite area of Kuala Lumpur and the property is developed by one of top developers in Klang Valley some more! Best of the best, I can stop “helping stranger to pay house installment” soon! In case you don’t get it, I am trying to say I will no longer pay rent when my property is ready as I am currently renting a room while working in Kuala Lumpur. Anyway, 3 more years to go before I get the house key 🤣